The rapid expansion of artificial intelligence, cloud computing, and global data infrastructure has ushered in a new industrial era—one dominated not by smokestacks, but by server farms. Yet behind the sleek image of digital technology lies a very physical reality: vast data centers made from concrete and steel. These materials, essential to modern construction, are among the most carbon-intensive products on Earth.

Cement alone accounts for roughly 6–8% of global greenhouse gas emissions, while steel contributes another major share. Combined, these industries represent a significant portion of global emissions, making them critical targets in the fight against climate change.

As companies like Microsoft, Amazon, and Google build thousands of data centers to support AI and cloud services, their demand for cement and steel is skyrocketing. This surge has caused emissions to rise—even as these same companies pledge to reach net-zero or carbon-negative targets.

The result is a paradox: Big Tech is both accelerating emissions through infrastructure expansion and leading the charge to eliminate them. This article explores how these companies plan to decarbonize cement and steel production—and reshape two of the world’s hardest-to-clean industries.

Why Cement and Steel Are So Hard to Decarbonize

The Chemistry Problem

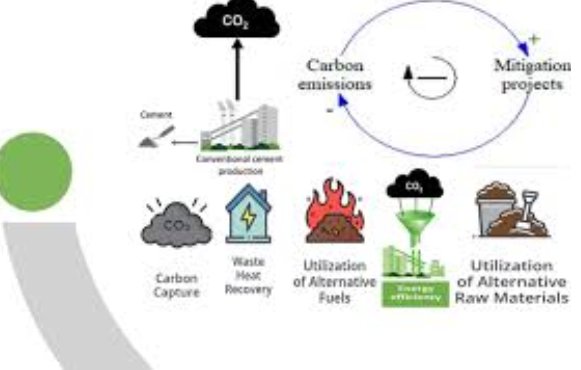

Unlike electricity generation, where emissions can be reduced by switching to renewable energy, cement production emits carbon dioxide as part of its core chemical process. Limestone is heated in kilns at extremely high temperatures, releasing CO₂ through a reaction known as calcination.

Steel production faces a similar challenge. Traditional methods rely on coal-fired blast furnaces to extract iron from ore, making it one of the most energy- and carbon-intensive industrial processes.

The Scale Problem

Cement and steel are foundational materials used in nearly every building, bridge, and piece of infrastructure. Demand is massive and still growing—especially with the global construction boom driven by urbanization and digital infrastructure.

The Cost Problem

Low-carbon alternatives often remain more expensive than traditional methods. Without strong demand signals or policy support, manufacturers have little incentive to switch.

This is where Big Tech enters the picture—not just as a consumer, but as a catalyst.

Big Tech’s Role as a Market Maker

Creating Demand for Green Materials

One of the most powerful tools Big Tech possesses is its purchasing power. By committing to buy low-carbon cement and steel at scale, companies can create guaranteed demand that encourages manufacturers to invest in cleaner technologies.

For example, Microsoft has signed long-term agreements to purchase low-carbon cement, helping startups scale production and reduce costs over time.

Similarly, Amazon and other tech giants are forming coalitions and partnerships to signal demand for sustainable materials across the industry.

These “offtake agreements” are crucial. They reduce financial risk for innovators and accelerate commercialization of new technologies.

Strategy 1: Investing in Low-Carbon Cement Technologies

Electrochemical Cement Production

Traditional cement relies on fossil-fuel-powered kilns. New approaches, such as electrochemical processes, eliminate combustion entirely. These methods use electricity—potentially from renewable sources—to produce cement without releasing CO₂ from fuel burning.

Microsoft’s partnership with emerging cement innovators demonstrates how Big Tech is supporting these breakthroughs. By committing to future purchases, it enables companies to build large-scale production facilities.

Alternative Materials and Mixes

Another approach involves reducing the amount of clinker (the most carbon-intensive component of cement) by substituting it with alternative materials such as:

- Fly ash (a byproduct of coal combustion)

- Slag from steel production

- Biogenic limestone produced using algae

Pilot projects have shown that these alternative mixes can cut emissions by more than 50% compared to traditional concrete.

Carbon-Negative Cement

Some startups are developing cement that actually absorbs CO₂ during production or curing. While still in early stages, these technologies could transform cement from a major emitter into a carbon sink.

Strategy 2: Decarbonizing Steel Production

Green Hydrogen Steel

One of the most promising innovations in steelmaking is the use of hydrogen instead of coal. When hydrogen is used to reduce iron ore, the only byproduct is water vapor instead of carbon dioxide.

Big Tech companies are investing in projects that support hydrogen-based steel production, either directly or through supply chain partnerships.

Electric Arc Furnaces (EAFs)

Recycling steel using electric arc furnaces powered by renewable energy significantly reduces emissions compared to traditional blast furnaces. Increasing the share of recycled steel is a key strategy.

ResponsibleSteel and Certification Systems

Tech companies are also pushing for industry standards that define what qualifies as “low-carbon steel.” These frameworks help ensure transparency and accountability across supply chains.

Strategy 3: Environmental Attribute Certificates (EACs)

One of the most innovative tools emerging in this space is the use of Environmental Attribute Certificates (EACs).

How EACs Work

EACs allow companies to claim emissions reductions by financially supporting low-carbon production—even if the physical materials are not directly used in their projects.

For example, Microsoft has developed a framework for certifying low-carbon cement and steel, ensuring that purchases lead to real, measurable emissions reductions.

Why They Matter

EACs solve several key challenges:

- Geographic limitations in sourcing green materials

- Supply shortages of low-carbon products

- High upfront costs for new technologies

By creating a flexible market mechanism, EACs accelerate adoption and scale.

Strategy 4: Direct Investment in Startups

Big Tech is not just buying green materials—it is funding their development.

Climate Innovation Funds

Companies like Microsoft have launched dedicated climate funds to invest in startups working on:

- Low-carbon cement

- Carbon capture technologies

- Advanced materials science

These investments help bridge the “valley of death” between research and commercialization.

Strategic Partnerships

Amazon, for instance, has invested in companies developing technologies to reduce emissions in concrete production and has begun using low-carbon concrete in its data centers.

Such partnerships provide startups with capital, expertise, and access to large-scale deployment opportunities.

Strategy 5: Collaborative Industry Initiatives

Coalitions and Alliances

Big Tech companies are joining forces through initiatives like:

- Sustainable Concrete Buyers Alliance

- Open Compute Project collaborations

These groups aim to standardize requirements, pool demand, and accelerate innovation.

By acting collectively, companies can send stronger market signals and reduce fragmentation.

Public-Private Partnerships

Governments also play a role by providing funding, regulations, and incentives. While policy support has fluctuated, collaboration between public and private sectors remains essential for scaling solutions.

Strategy 6: Carbon Capture and Storage (CCS)

Capturing Emissions at the Source

Carbon capture technology can be applied to cement and steel plants to trap CO₂ before it enters the atmosphere. The captured carbon can then be stored underground or used in other applications.

Although expensive, CCS is considered essential for decarbonizing heavy industries where emissions are unavoidable.

Integration with Tech Supply Chains

Big Tech companies are exploring ways to integrate CCS into their supply chains, either by sourcing from facilities that use it or investing in its development.

Strategy 7: Designing Low-Carbon Data Centers

Material Efficiency

Reducing the amount of cement and steel used in construction is another key strategy. This includes:

- Optimized structural designs

- Modular construction techniques

- Use of alternative materials

Lifecycle Thinking

Companies are increasingly considering the entire lifecycle of their buildings—from construction to operation to decommissioning.

Amazon, for example, emphasizes both construction materials and operational efficiency in its decarbonization strategy.

The Role of Artificial Intelligence

Ironically, the same AI driving demand for data centers is also helping reduce emissions.

Process Optimization

AI can optimize manufacturing processes in cement and steel plants, improving energy efficiency and reducing waste.

Supply Chain Transparency

Advanced analytics help track emissions across complex global supply chains, enabling better decision-making.

Challenges and Limitations

Scaling Issues

Despite rapid innovation, low-carbon cement and steel currently represent a tiny fraction of global production. Scaling up will take time and significant investment.

Cost Barriers

Green materials often come with a price premium. While Big Tech can afford to pay more, widespread adoption will require cost reductions.

Policy Uncertainty

Government support is inconsistent, and regulatory frameworks are still evolving. This creates uncertainty for investors and manufacturers.

Rising Demand

The biggest challenge may be demand itself. As AI and cloud computing expand, the need for new data centers—and the materials to build them—continues to grow rapidly.

The Bigger Picture: Transforming Heavy Industry

Big Tech’s efforts go beyond reducing its own carbon footprint. By investing in cement and steel decarbonization, these companies are helping transform entire industries.

Their influence extends across global supply chains, affecting:

- Construction practices

- Manufacturing standards

- Investment flows

In effect, Big Tech is acting as a bridge between innovation and large-scale deployment.

Conclusion: A New Industrial Revolution

The decarbonization of cement and steel represents one of the greatest challenges—and opportunities—of the 21st century. These industries are deeply embedded in the global economy, yet they are also among the most difficult to clean up.

Big Tech companies are uniquely positioned to drive change. Through their massive purchasing power, technological expertise, and willingness to invest in innovation, they are accelerating the transition to low-carbon materials.

The path forward will not be easy. It requires collaboration across industries, governments, and communities. It demands new technologies, new business models, and new ways of thinking about infrastructure.

But if successful, these efforts could mark the beginning of a new industrial revolution—one where the foundations of our digital world are no longer built on carbon, but on sustainability.